Introduction: Understanding FBAR Reporting Requirements

The Foreign Bank Account Report (FBAR), or FinCEN Form 114, is a critical reporting requirement for U.S. persons with financial interests in or signature authority over foreign financial accounts. Suppose you have foreign bank accounts, investment accounts, or other financial holdings outside the United States that exceed $10,000 in aggregate at any point during the calendar year. In that case, you must file an FBAR with the Financial Crimes Enforcement Network (FinCEN).

FBAR compliance isn't merely a suggested practice—it's a mandatory requirement under the Bank Secrecy Act designed to combat tax evasion and money laundering through offshore accounts. With increased information sharing between financial institutions globally and heightened scrutiny from U.S. tax authorities, proper FBAR filing has never been more critical.

In this comprehensive guide, I'll walk you through the entire FBAR filing process, from determining your reporting obligations to submitting your FinCEN Form 114. Whether you're a first-time filer or seeking to ensure your existing compliance practices are current, this step-by-step approach will help you navigate the complexities of foreign account reporting and avoid potentially severe penalties.

Who Needs to File FBAR: Understanding Your Obligations

Defining "U.S. Persons" for FBAR Purposes

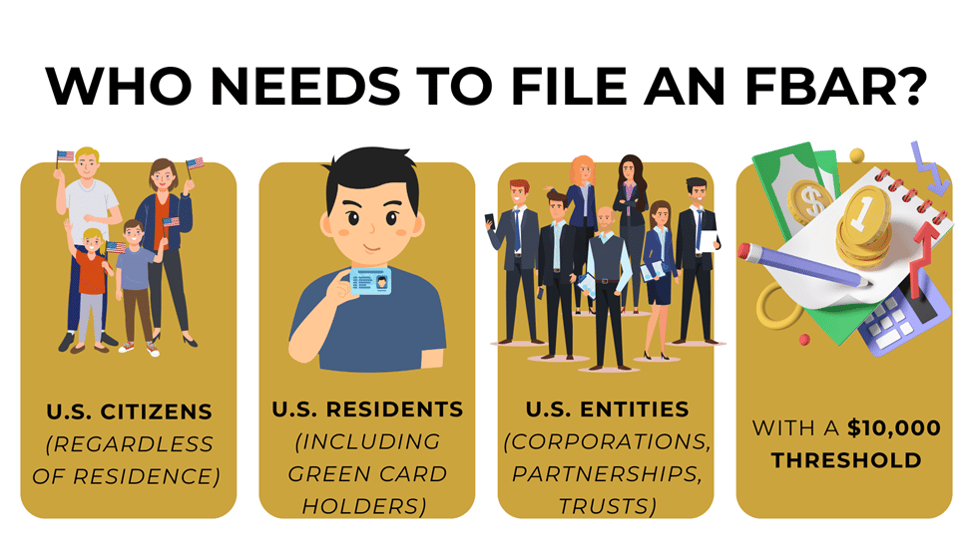

FBAR filing requirements apply to "U.S. persons," which include:

- U.S. citizens (including those residing abroad)

- U.S. residents (including green card holders)

- Entities such as corporations, partnerships, and trusts formed under U.S. law or with a principal place of business in the United States

The definition is intentionally broad to capture all individuals and entities with potential foreign financial ties.

The $10,000 Threshold Explained.

You must file an FBAR if the aggregate value of all your foreign financial accounts exceeds $10,000 at any time during the calendar year. This critical point catches many taxpayers off guard—the requirement is based on the combined maximum value of all accounts, not each account.

For example, if you have three foreign accounts with maximum balances of $4,000, $5,000, and $2,000, respectively, your aggregate maximum equals $11,000, exceeding the threshold and triggering the filing requirement. The combined value matters even if each account individually falls below $10,000.

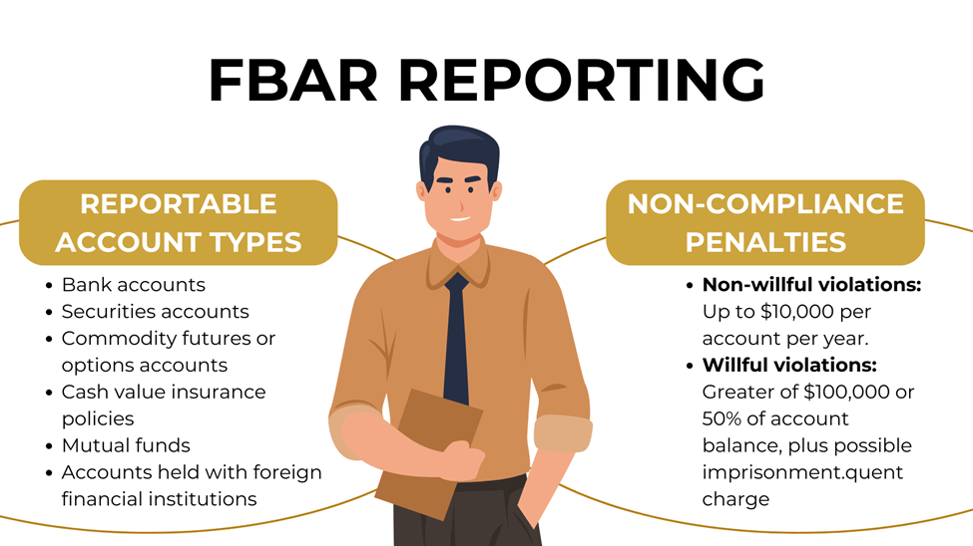

Reportable Account Types

FBAR reporting covers a wide range of financial accounts held outside the United States:

- Bank accounts (savings, checking, time deposits)

- Securities accounts (brokerage accounts, investment portfolios)

- Commodity futures or options accounts

- Insurance policies with cash value (such as whole life insurance)

- Mutual funds or similar pooled funds

- Foreign Pension Accounts

- Other accounts maintained with foreign financial institutions

Non-Compliance Penalties: What's at Stake

Failing to meet FBAR filing obligations can result in substantial penalties that underscore the importance of compliance:

- Non-willful violations: Up to $10,000 per one year when the rules are violated

- Willful violations: The greater of $100,000 or 50% of the account balance at the time of the breach, plus potential criminal charges, including imprisonment for up to 5 years

These penalties highlight why proper FBAR filing should be a priority for anyone with foreign financial accounts. Even if your foreign accounts generate no income or tax liability, the FBAR filing requirement still applies.

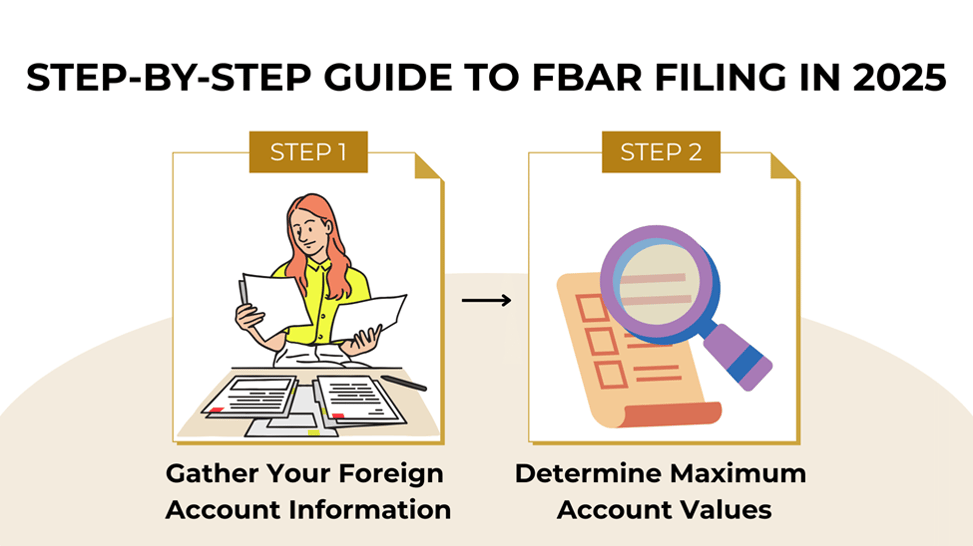

Step-by-Step Guide to FBAR Filing in 2025

Step 1: Gather Your Foreign Account Information

Before beginning the filing process, collect the following information for each foreign financial account:

- Financial institution details:

- Official name of the financial institution

- Complete address, including postal code

- Institution's identification number (if applicable)

2. Account information:

- Account number or other identifier

- Type of account (bank, securities, etc.)

- Whether the account was opened or closed during the reporting year

3. Maximum value:

- The maximum value of the account during the calendar year

- For accounts in foreign currency, the exchange rate used for conversion to USD

4. Difficulties encountered:

- If you encounter difficulties in obtaining values, please use your available sources of information to estimate the balance. Always stay on the conservative side when estimating the figures.

Step 2: Determine Maximum Account Values

For each account, you'll need to report the maximum value during the calendar year converted to U.S. dollars:

- Review all account statements to identify the highest balance during the year (not just the year-end balance)

- Convert the maximum value to USD using the Treasury's Financial Management Service rate for December 31 of the reporting year

- For accounts in multiple currencies, convert each maximum value separately

- Document your methodology and retain records of the conversion calculations

Step 3: Access the BSA E-Filing System

FBAR filing must be done electronically through FinCEN's BSA E-Filing System:

- Visit the BSA E-Filing website at https://bsaefiling.fincen.treas.gov/

- For individual filers, select "File FinCEN Form 114 individually" under the "No Registration FBAR Filer" option

- For entities or preparers filing for clients, register for a BSA E-Filing account to obtain a User ID and password

Step 4: Complete FinCEN Form 114 Section by Section

Navigate through the form methodically to ensure all required information is properly reported:

Part I: Filer Information

- Enter your personal identifying information (name, Social Security Number, date of birth)

- Indicate the type of filer (individual, partnership, corporation, etc.)

- Specify whether this is a consolidated report for a business entity

Part II: Information on Financial Account(s) Owned Separately

- Provide your contact information (address, phone number)

- Use specific formats for address fields and phone numbers

- List the number of accounts being reported

Part III: Information on Financial Account(s) Owned Jointly

- For each account, provide the institution name, address, and account number

- Specify the account type (bank, securities, etc.)

- Enter the maximum value during the reporting year in USD

- Indicate if other individuals have a financial interest in the account

Part IV: Information on Financial Account(s) Where Filer Has Signature Authority

- Report accounts where you have signature authority but no financial interest

- Include the account owner's information along with account details

Part V: Information on Financial Account(s) Owned by U.S. Person With Financial Interest

- Complete this section if you're filing as having a financial interest in 25 or more accounts

- Provide summary information about the accounts

Step 5: Review for Accuracy and Submit

Before submitting your FBAR:

- Double-check all entered information, paying special attention to:

- Account numbers

- Maximum values and currency conversions

- Contact information

- Institution details

- Carefully review the signature section, understanding that you're signing under penalty of perjury

- Click "Submit" to electronically file your FBAR

- Save and print the confirmation page showing your BSA Identifier number for your records

Step 6: Maintain Proper Records

After filing, maintain comprehensive records for at least five years from the due date:

- Copies of filed FBARs with confirmation numbers

- Account statements showing balances throughout the year

- Documentation of the exchange rates used

- Any correspondence with FinCEN regarding your filings

Special Considerations for FBAR Filing

Southeast Asian Accounts: Regional Complexities

For U.S. persons with accounts in Southeast Asian countries, several unique considerations apply:

- Availability of Account Information: You may encounter difficulties obtaining the six-year data from your local banks in your home country. Do not despair. Use your best estimate for the information if there are no other ways to obtain the information.

- Currency fluctuations: Southeast Asian currencies can experience significant volatility, affecting the USD conversion and potentially pushing accounts over the $10,000 threshold

- Different account structures: Many Southeast Asian financial institutions offer account types that don't precisely match U.S. categories, requiring careful assessment for proper reporting

- Naming conventions: Account holder names may be formatted differently in Southeast Asian countries, creating potential matching issues with U.S. documentation

I recommend maintaining detailed records of how Southeast Asian accounts are categorized and valued to ensure consistent reporting across tax years.

Addressing Late FBAR Filings

If you've missed previous FBAR filing deadlines:

- Delinquent FBAR Submission Procedure: For non-willful violations with no unreported income, file past-due FBARs electronically through the BSA E-Filing System with a statement explaining the reason for late filing

- Streamlined Filing Compliance Procedures: For U.S. taxpayers residing abroad who non-willfully failed to file, this program offers reduced penalties and simplified compliance procedures

- Voluntary Disclosure Program: For cases with potential willful violations, the IRS Criminal Investigation Voluntary Disclosure Practice may provide protection from criminal prosecution

You should consider consulting with a tax professional specializing in international compliance before pursuing any of these remediation options.

Important FBAR Deadline Information for 2025

For the 2024 calendar year, FBAR filing is due April 15, 2025, with an automatic extension to October 15, 2025, without requiring a specific extension request. However, I recommend filing as soon as possible rather than waiting for the extension deadline, as early filing demonstrates good-faith compliance efforts.

Conclusion: Ensuring FBAR Compliance for Peace of Mind

Navigating FBAR filing requirements can seem daunting, but following this step-by-step guide will help ensure you meet your foreign account reporting obligations while minimizing the risk of costly penalties. Remember that the FBAR is filed separately from your tax return and has its own distinct requirements and deadlines.

Key takeaways for successful FBAR filing include:

- Understand whether you meet the threshold for filing (aggregate foreign accounts exceeding $10,000)

- Gather comprehensive information about all foreign financial accounts

- File electronically through the BSA E-Filing System before the deadline

- Maintain detailed records for at least five years after filing

- Consider professional assistance for complex situations

At CHI border Tax Advisory, we specialize in helping U.S. persons navigate the complexities of international tax compliance. Our team can provide personalized guidance tailored to your specific circumstances.

Don't leave your FBAR compliance to chance. Schedule a complimentary consultation with Chi Border Tax Advisory today to ensure your foreign account reporting meets all requirements and protects you from potential penalties.

Disclaimer: The information provided in this article is for general informational purposes only and should not be construed as professional tax advice. Tax laws and regulations are complex and subject to change. While we strive to provide accurate and up-to-date information, individual circumstances vary, and you should consult with a qualified tax professional regarding your specific situation.